Provision Summary:

Provision Summary:

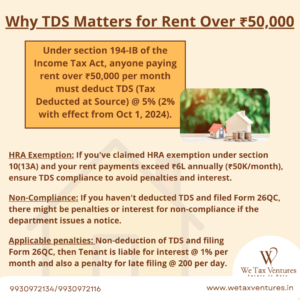

Under Section 194-IB of the Income Tax Act, individuals or Hindu Undivided Families (HUFs) not liable to tax audit must deduct TDS when rent paid exceeds ₹50,000 per month.

Example:

If you pay ₹60,000/month rent, total annual rent = ₹7,20,000

TDS = 5% of ₹7,20,000 = ₹36,000

You deduct and deposit ₹36,000 to the government, and pay the rest to the landlord

Consequences of Non-Compliance:

Interest for late deduction/deposit

Penalties

Disallowance of expenses under income tax assessment

| Criteria | Details |

| Applicable Section | Section 194-IB |

| Who needs to deduct TDS | Individual or HUF (not under tax audit) |

| Threshold Limit | Rent > ₹50,000 per month |

| TDS Rate | 5% |

| PAN of Landlord | Required – if not available, TDS at 20% |

| When to Deduct TDS | Once during the financial year (typically in the last month of tenancy or March) |

| TAN Requirement | Not required |

| Form to be filed | Form 26QC (challan-cum-statement) |

| TDS Certificate | Form 16C (to be issued to landlord) |

| Due Date to Deposit TDS | Within 30 days from the end of the month in which TDS is deducted |