Section 115BAC of the Income Tax Act, 1961, introduces the new tax regime in India. It offers concessional tax rates for individuals

and Hindu Undivided Families (HUFs), with the condition of foregoing most exemptions and deductions available under the old regime. The aim is to simplify tax compliance while offering flexibility to taxpayers.

🔍 Who Can opt for Section 115BAC?

Individuals (Resident & Non-Resident)

HUFs

Association of Persons (AOP)

Body of Individuals (BOI)

Artificial Juridical Persons (AJP)

What are the new income tax slabs under the New Tax Regime for FY 2025–26?

The tax slabs under the new regime for the financial year 2025-26 are as follows

| Total Income (₹) | Tax Rate |

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

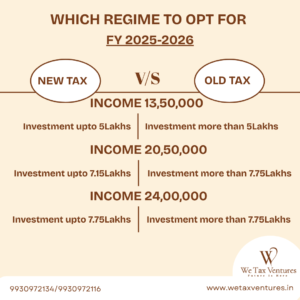

🤔 Old vs New Tax Regime – Which One Should You Choose?

| Criteria | Old Regime | New Regime (115BAC) |

| Tax Slabs | Higher | Lower |

| Deductions Allowed | Yes (80C, 80D, HRA, etc.) | Mostly not allowed |

| Standard Deduction | Yes (₹50,000) | Yes (from FY 2023-24) |

| Simplicity | Complex due to exemptions | Simpler with fewer claims |

| Best For | Individuals with high deductions | Individuals with no/low deductions |

Additionally, a tax rebate of up to ₹60,000 is available for individuals with income up to ₹12 lakh, effectively making their tax liability zero.

Key Takeaways

Section 115BAC offers lower tax rates but fewer deductions.

It is the default tax regime from FY 2023-24.

Analyze your income, investments, and exemptions before choosing the regime.

Is the New Tax Regime now the default option?

Yes, as per the Finance Act 2024, the New Tax Regime is the default for individuals, Hindu Undivided Families (HUFs), Associations of Persons (AOPs), and other entities. However, taxpayers can opt for the Old Tax Regime if they prefer.

Can I still claim deductions like HRA and 80C under the New Regime?

No, the New Tax Regime offers lower tax rates but restricts most exemptions and deductions, including

-

House Rent Allowance (HRA)

-

Section 80C (e.g., investments in PPF, ELSS)

-

Section 80D (medical insurance)

-

Home loan interest under Section 24(b)

However, the standard deduction of ₹75,000 is available.

Should I choose the New or Old Tax Regime?

The choice depends on your individual financial situation:

-

If you have significant deductions (e.g., home loan interest, investments under 80C), the Old Regime might be more beneficial.

-

If you have fewer deductions, the New Regime’s lower tax rates could result in tax savings.

It’s advisable to use the Income Tax Department’s calculator to compare both regimes.

Do I need to inform my employer about my chosen tax regime?

Yes, employees must inform their employers about their preferred tax regime. If no intimation is made, the employer will deduct tax based on the default New Regime. However, the final choice can be made when filing the income tax return.

Are life insurance policies still beneficial under the New Regime?

Under the New Regime, the tax-saving benefits of life insurance policies (under Section 80C) are not applicable. Therefore, if the primary purpose of holding such policies was tax savings, you might want to reassess their relevance in your financial portfolio.

🔎 FAQs on Section 115BAC

Q1. Can I claim 80C under Section 115BAC?

❌ No, deductions under 80C are not allowed in the new tax regime.

Q2. Is standard deduction allowed under the new tax regime?

✅ Yes, from FY 2023-24, ₹50,000 standard deduction is allowed for salaried and pensioners.

Q3. How to switch back to the old regime?

You can opt in or out while filing your ITR, except for those with business/professional income, who must stick to their choice once exercised.

If you need assistance in comparing the tax liability under both regimes based on your income and investments, feel free to ask!